Revolutionizing

Travel Payments

Unlock working capital and discover new revenue streams with virtual cards for OTAs, airlines, and hotels

Join 1000+ companies on the Nium payments infrastructure

Travel

Your ticket to optimizing payments

For online travel agencies, slow, high-risk payments are eating into shrinking profit margins. Reconciliation and settlement delays are also creating funding gaps that can shut down business. To effectively pay airlines, hotels, and the global travel ecosystem, Nium payment solutions—featuring broad virtual credit card support—help travel intermediaries maximize profitability.

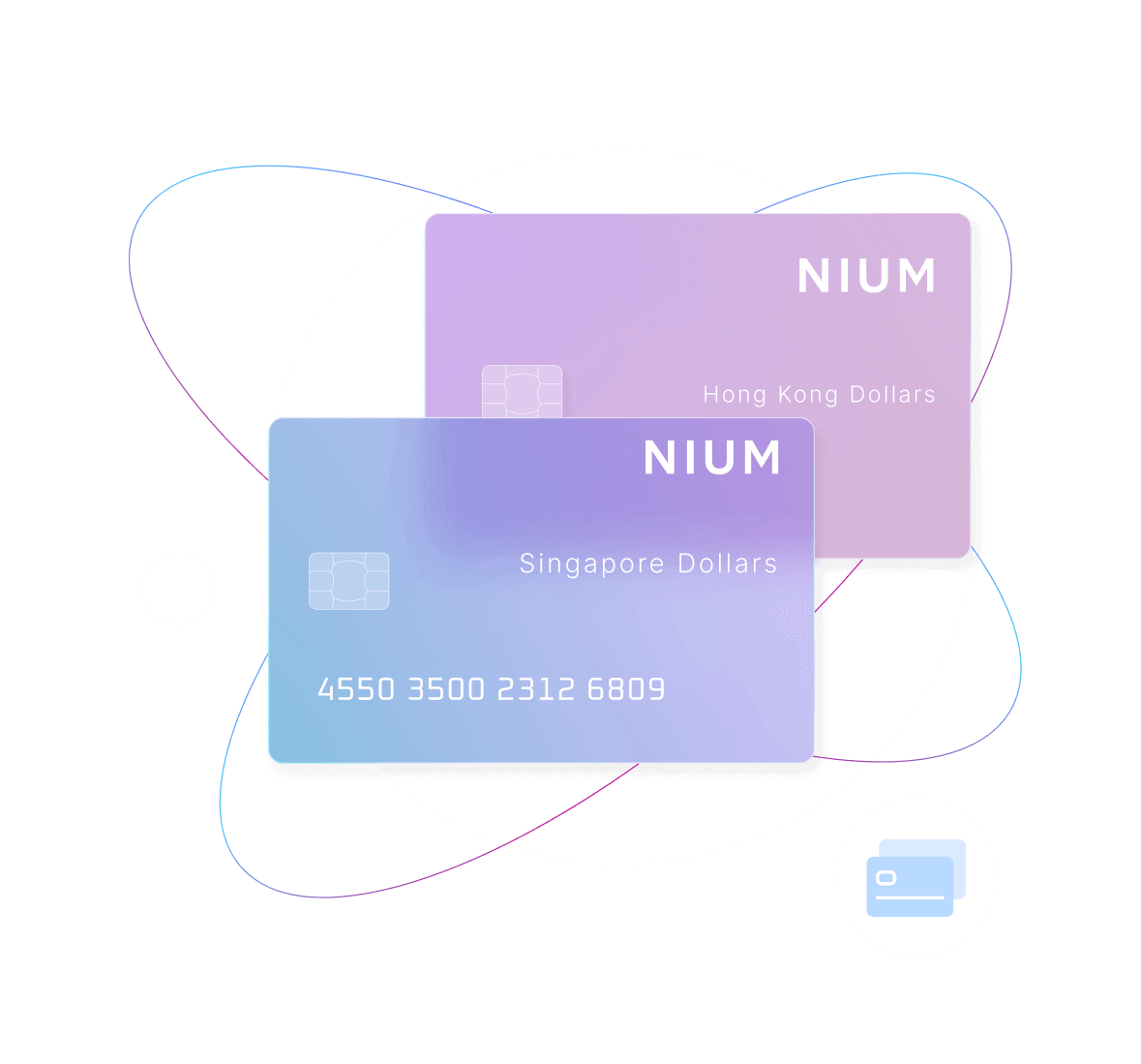

Add global

virtual credit

card capabilities

-

Extensive portfolio of Mastercard and Visa cards

Find the perfect mix of rewards, acceptance, and merchant fees that work best for your use case and jurisdiction.

-

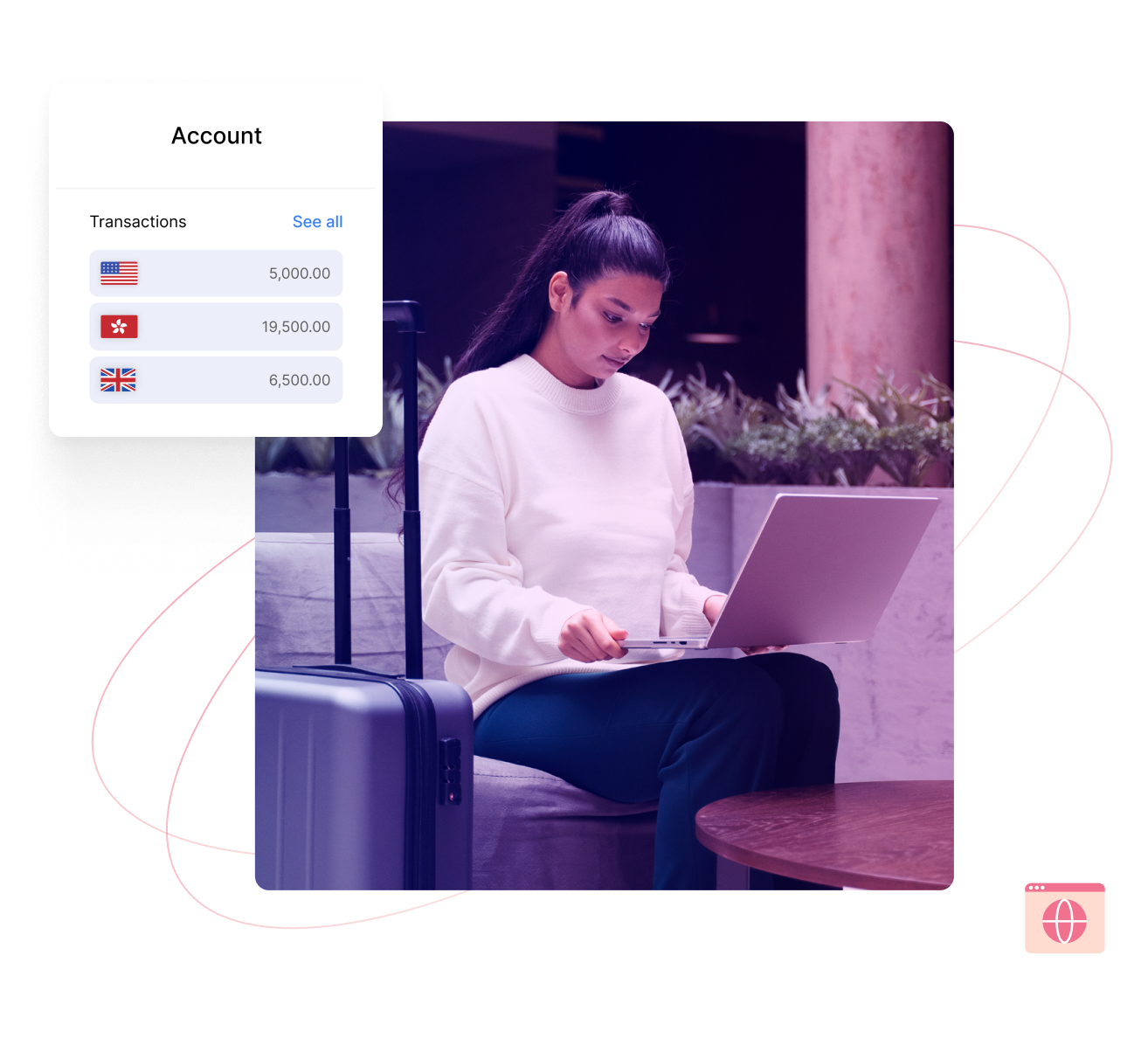

Fund and issue virtual travel cards in 20+ currencies

Lower the cost of foreign exchange conversions and improve acceptance all over the world.

-

Modern ways to send wires

Design transparent incentives for OTA partners based on routes, seasonality, business volumes, and more.

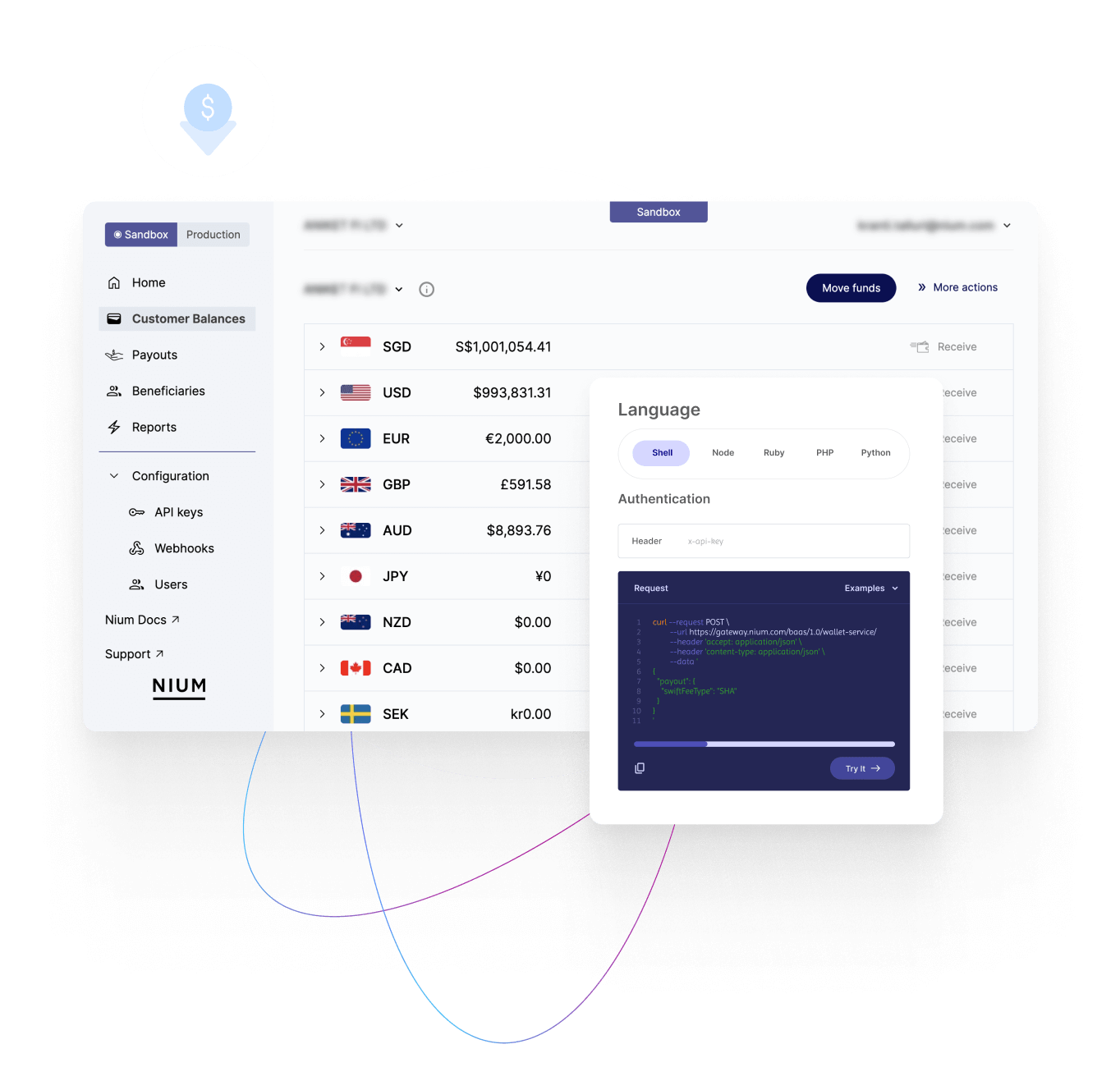

Supported currencies

Create and manage bank accounts in 20+ currencies with one API

Use payments to drive revenue and working capital

-

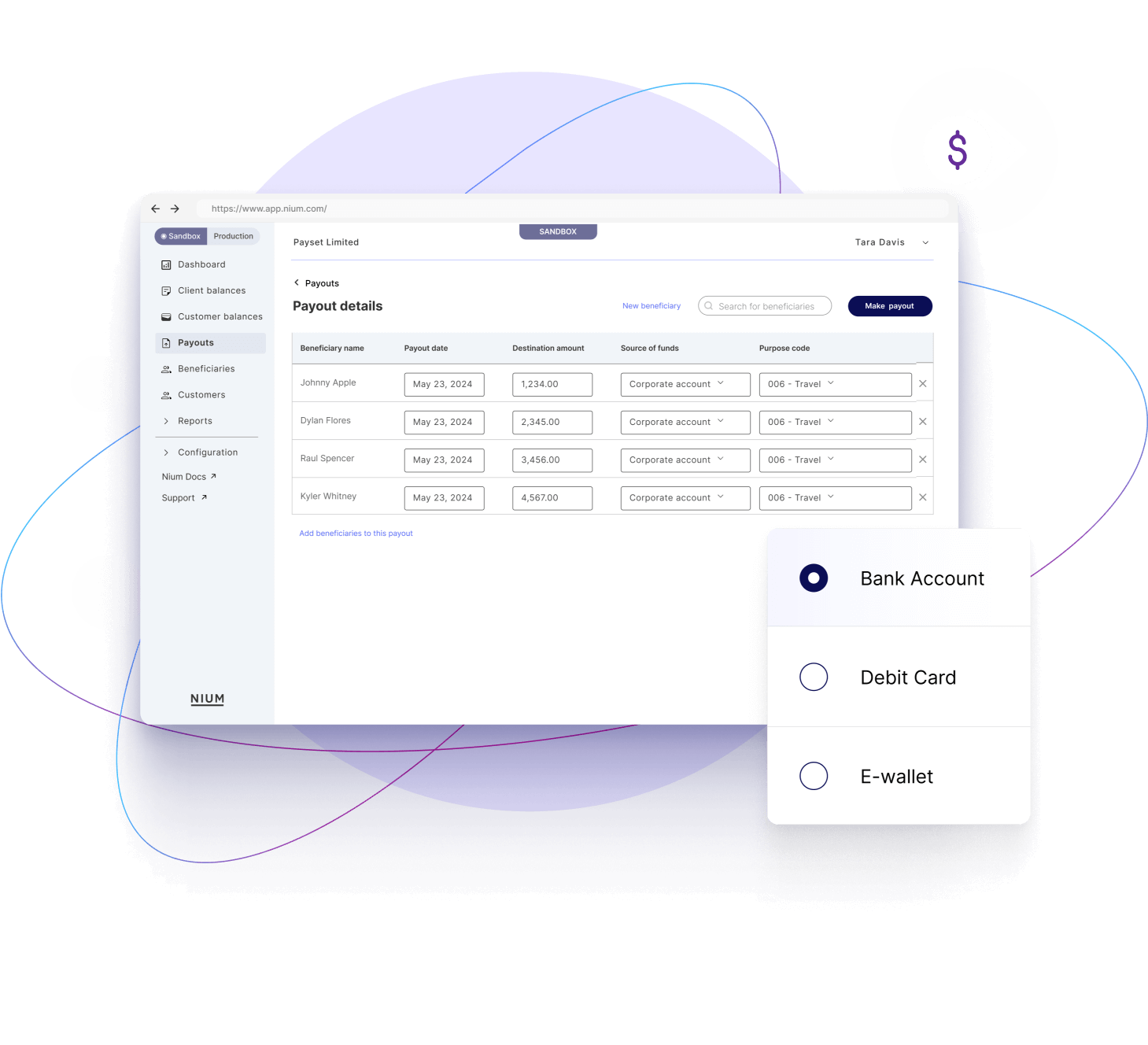

Get end-to-end control over cash flow

Customize specific payment account parameters, such as the amount, the payee, and the time of payment.

-

Settle invoices in 2 days instead of 30

Improve relationships with merchants and airlines and clear the way for travel commerce.

-

Generate revenue and reduce margin erosion

Nium preempts regulatory changes and easily maximizes or reduces interchange to reduce risk and improve supplier relationships

Layers of protection to reduce risk

-

Full chargeback protection by Visa and Mastercard

If a merchant doesn’t provide the promised service, businesses dispute charges and reclaim funds.

-

Reduce fraud with virtual card numbers

More secure than traditional physical cards, single-use and multi-use card numbers can be designated for specific transactions and can be deactivated after payment.

-

Lock out rogue spend with merchant category codes (MCCs)

Nium provides OTAs with a broad range of MCCs to limit how and where the virtual cards can be used.

First-class round trips for your payment data

-

Highly customizable, comprehensive reports

Reports include card activity, funding, non-zero card balance, scheduled loads, and balance sheet.

-

Easily customize up to 20 data fields

Attach booking references for every transaction to bring rich data to your financial and BI systems to identify ways to increase margins and reduce costs.

-

Automated reconciliation processes

Get clean transaction data and eliminate errors associated with manual reconciliation.

Hear From Our Customers

“We chose Nium for its advanced technology and broad payouts reach in 190+ countries around the world including some of the most mature economies such as China, Hong Kong, the U.S. and the U.K. That, combined with the real-time speed of their payments at considerably lower transaction costs compared to older global payment rails like Swift, and the company’s broad market knowledge in emerging and established markets, makes it an ideal partner to handle payouts abroad from Brazil to the rest of the world.”

– Rodrigo Xavier, CEO of OZ Câmbio

Watch now →

"We currently live in a borderless world with a strong sense of urgency where we see customers focused on three pillars, reliability, state of the art technology, and most importantly, real time payments and instant payments."

- Mauro Neto, New product development, Treviso

Watch now →

Nium’s solution has helped KBank grow and give a better service to our customers. Nium’s solution improves every year, and we are looking forward to expanding to more corridors in the future.

– Tawan Thammanichanon, Head of International Trade Product Management at KBank

Watch now →Premium content

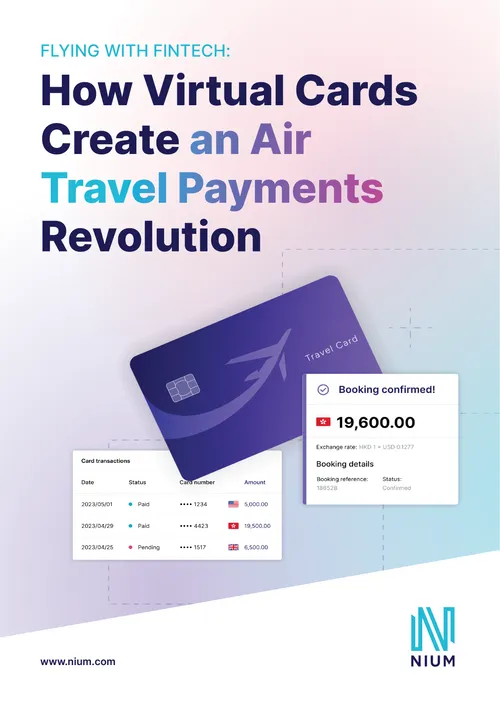

Flying With Fintech: How Virtual Cards Create an Air Travel Payments Revolution

Resources

Let's Meet!

Events Calendar

Read more

Frequently Asked Questions

-

Which currencies does Nium offer for issuing and funding?

EUR, GBP, USD, AUD, CAD, CHF, CZK, DKK, HKD, HUF, ILS, JPY, MXN, NOK, NZD, PLN, RON, SEK, SGD, THB, TRY, ZAR, AED

-

What benefits do Nium Virtual Credit Cards provide?

By using Nium Virtual Credit Cards you can balance incentives and cash flow while optimizing every payment that you make. That allows you to:

- Unlock working capital

- Increase card acceptance rates

- Manage your FX exposure with 20+ funding and issuing currencies

- Simplify chargeback processing

- Automate booking reconciliation

-

Does Nium provide consumer virtual credit cards?

No, the Nium Virtual Credit Cards can be used for B2B travel payments only.

-

How many funding currencies does Nium offer?

Nium offers 20+ funding currencies

-

How can Nium help me optimize my travel payments?

Nium combines flexible funding methods with an industry-leading scheme-agnostic portfolio of virtual cards. Our team of optimization specialists helps the world’s leading travel brands leverage this powerful technology to maximize rewards from every payment and increase travel margins.

The Global Infrastructure For Real-Time Payments

Nium moves money, manages foreign exchange, and mitigates fraud so your business can send and receive funds in real-time.

Let’s talk!

Interested?

Talk with our representatives to get onboard

Contact Nium's experts to build innovations, get unparalleled technical and account support and get customized pricing and packages.

190+

Payout countries

and territories

100+

Real-time

markets

100+

Supported

currencies

75M

Cards issued

worldwide